Foreign direct investment (FDI) in India grew by 14% to a record of $ 49.8 billion in the 2019-20 financial year, according to data by the Department for Promotion of Industry and Internal Trade (DPIIT).

Total FDI, (which includes equity capital of unincorporated bodies, reinvested earnings and other capital) rose by 18 % to $73.4 billion in the same year.

FDI had contracted by 1 % in the year 2018-19 and grew by 3 % in 2017-18.

[You may also read- Types of Foreign Investment Decoded- FDI, FII, FPI and QFI]

This is the highest growth in FDI in 4 years. Refer the table below

| Year | FDI Growth |

| 2014-15 | 22 % |

| 2015-16 | 35 % |

| 2016-17 | 9 % |

| 2017-18 | 3 % |

| 2018-19 | -1 % |

| 2019-20 | 14 % |

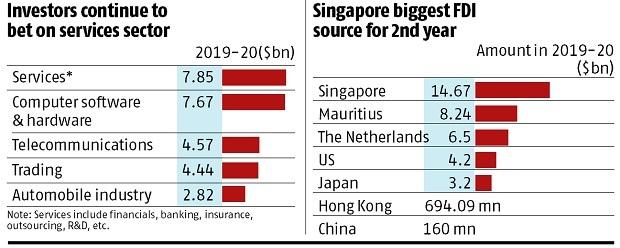

Services sector ( which includes financial, banking, insurance, and outsourcing and others) was the highest recipient of FDI. This was followed by Computer software & hardware, Telecommunications, Trading, and Automobile industry in that order. (Refer the table below)

Singapore was the largest source of FDI in India in 2019-20. It was on the top spot in 2018-19 as well.

Since the year 2000, Mauritius has always been the top source of FDI inflows into India. In 2015-16, its position was replaced by Singapore. But, in 2016-17 and 2017-18, Mauritius regained the top spot, before being replaced again in 2018-19.

Singapore and Mauritius are mostly used to route capital from other countries into India. Consider that the largest investment in 2018-19 was Walmart’s Singapore based entity buying out 77 % on Flipkart for $16 billion

In the case of Mauritius… almost all of the identified flows are in fact routed, while in the case of Singapore this touches 90%. (10 % are direct FDI)

Source: //thewire.in

A part of the reason is, these countries are tax havens.

For years, Mauritius dominated because of two reasons-

- Mauritius is a tax haven. Apart from lower corporate taxes, there is no capital gains tax imposed by Mauritius.

- To add to the above, India had signed a Double Taxes Avoidance Agreement (DTAA) with Mauritius in 1982. As per the treaty, capital gains for the transfer of shares in India by a Mauritius-based company investing in India will be taxed in Mauritius. Since there is no capital gains tax in Mauritius, capital gains in India become exempt. [I’d highly recommend you to read- The India-Mauritius Treaty Amendment Explained]

- It is very easy to acquire residential status in Mauritius. A company just needs to have a post-box address to be a resident of Mauritius. So, it becomes easy to set up shell companies (that exist only on paper) in the country and invest in Indian equity to avoid paying capital gains tax.

Therefore, companies set up shell companies in Mauritius to route their capital investments into India to avoid paying taxes.

Mauritius has lost allure in the past few years and was replaced by Singapore because of the following reasons:

- India revised its treaty with Mauritius in May 2016. The amendments will come into full effect in 2019-20. As per the amendments, India will be allowed to impose capital gains on the transfer of Indian shares by companies based out of Mauritius. [It has to be noted that, India and Singapore had also revised its double tax avoidance agreement (DTAA) in 2016 to tax capital gains on investments from the country, but Singapore offers other advantages as well]

- Apart from being a tax haven, Singapore has other structural advantages like ease of doing business, developed infrastructure, strategic location in Asia, excellent Intellectual Property regime, economic and political stability, high quality of living, etc. Therefore, investors continue to base their entities in Singapore.

- Along with the above amendment to tax treaties, India passed legislation called General Anti-Avoidance Rule (GAAR) in 2016-17. As per this legislation, if an arrangement/ transaction lacks commercial substance (done solely with the purpose of avoiding taxes), it will not be considered as a valid permissible arrangement. The GAAR overrides the tax treaties with different countries. [I’d highly recommend you to this article- What is GAAR?]

- To prove commercial substance in a country, it must meet certain criteria like conducting its core income-generating activity from there, having an adequate number of qualified employees in the country, and demonstrating adequate expenditure in the country proportionate to the level of activity carried out there. It’s easier to create substance in Singapore because Singapore has a well-established regulatory environment, banking facilities, and easier access to funds, as well as human resource talent. [Source: straitstimes.com]

Lastly, it has to be noted that FDI is routed through Netherland and Cyprus as well. But, in 2016, the Government had amended its tax treaty with Cyprus. However, the treaty with the Netherlands still provides significant tax advantages which are similar to that of Mauritius. It has become the third-biggest contributor of FDI into India. So, India has to plug these loopholes in its DTAAs with other countries as well.

However, FDI from China is low at $160 million. This year, in a move clearly directed towards China, India changed its Foreign Direct Investment (FDI) rules to curb opportunistic takeovers/ acquisitions of Indian companies amidst the COVID-19 pandemic. Even though FDI from China is relatively smaller in magnitude, India is wary of Chinese investors in strategic areas.

[You may also read: The Great Wall Against Chinese FDI]

Economyria is now on Telegram. For a simplified analysis of topics related to economy/ business/ finance, subscribe to Economyria on Telegram

But as per recent developments, Cayman Islands also figures in the list of top 10. The carrebean island has invested $3.67 bn, compared to $1bn of investment in the preceding year. What is your take on that ?